The tax brackets were updated this year, so your income may be taxed at a different rate than last year. Here are the updated brackets:

2021 tax rates:

If your filing status is Single:

2021 Income:

$0 - $9,950 = 10%

(Up $250 or 2.58% from $0 - $9,700 last year. See below for other 2020 rates and brackets)

$9,951 - $40,525 = 12%

$40,526 - $86,375 = 22%

$86,376 - $164,925 = 24%

$164,926 - $209,425 = 32%

$209,426 - $523,600 = 35%

$523,601 and over = 37%

(Up $13,300 or 2.58% from $510,301 and over last year)

See below for 2019 & 2020 tax rates and brackets

If your filing status is Married Filing Jointly (MFJ) or Qualifying Widow(er):

2021 Income:

$0 - $19,900 = 10%

$19,901 - $81,050 = 12%

$81,051 - $172,750 = 22%

$172,751 - $329,850 = 24%

$329,851 - $418,850 = 32%

$418,851 - $628,300 = 35%

$628,301 and over = 37%

If your filing status is Married Filing Separately (MFS):

2021 Income:

$0 - $9,950 = 10%

$9,951 - $40,525 = 12%

$40,526 - $86,375 = 22%

$86,376 - $164,925 = 24%

$164,926 - $209,425 = 32%

$209,426 - $314,150 = 35%

$314,151 and over = 37%

If your filing status is Head of Household (HH):

2021 Income:

$0 - $14,200 = 10%

$14,201 - $54,200 = 12%

$54,201 - $86,350 = 22%

$86,351 - $164,900 = 24%

$164,901 - $209,400 = 32%

$209,401 - $523,600 = 35%

$523,601 and over = 37%

2020 tax rates:

If your filing status is Single:

Income

$0 - $9,950 = 10%

$9,951 - $40,525 = 12%

$40,526 - $86,375 = 22%

$86,376 - $164,925 = 24%

$164,926 - $209,425 = 32%

$209,426 - $523,600 = 35%

$523,601 and over = 37%

If your filing status is Married Filing Jointly (MFJ) or Qualifying Widow(er):

Income

$0 - $19,900 = 10%

$19,901 - $81,050 = 12%

$81,051 - $172,750 = 22%

$172,751 - $329,850 = 24%

$329,851 - $418,850 = 32%

$418,851 - $628,300 = 35%

$628,301 and over = 37%

If your filing status is Married Filing Separately (MFS):

Income

$0 - $9,950 = 10%

$9,951 - $40,525 = 12%

$40,526 - $86,375 = 22%

$86,376 - $164,925 = 24%

$164,926 - $209,425 = 32%

$209,426 - $314,150 = 35%

$314,151 and over = 37%

If your filing status is Head of Household (HH):

Income

$0 - $14,100 = 10%

$14,101 - $53,700 = 12%

$53,701 - $85,500 = 22%

$85,501 - $163,300 = 24%

$163,301 - $207,350 = 32%

$207,350 - $518,400 = 35%

$518,401 and over = 37%

2019 tax rates:

If your filing status is Single:

Income

$0 - $9,700 = 10%

$9,701 - $39,475 = 12%

$39,476 - $84,200 = 22%

$84,201 - $160,725 = 24%

$160,726 - $204,100 = 32%

$204,101 - $510,300 = 35%

$510,301 and over = 37%

If your filing status is Married Filing Jointly (MFJ) or Qualifying Widow(er):

Income

$0 - $19,400 = 10%

$19,401 - $78,950 = 12%

$78,951 - $168,400 = 22%

$168,401 - $321,450 = 24%

$321,451 - $408,200 = 32%

$408,201 - $612,350 = 35%

$612,351 and over = 37%

If your filing status is Married Filing Separately (MFS):

Income

$0 - $9,700 = 10%

$9,701 - $39,475 = 12%

$39,476 - $84,200 = 22%

$84,201 - $160,725 = 24%

$160,726 - $204,100 = 32%

$204,101 - $306,175 = 35%

$306,176 and over = 37%

If your filing status is Head of Household (HH):

Income

$0 - $13,850 = 10%

$13,851 - $52,850 = 12%

$52,851 - $84,200 = 22%

$84,201 - $160,700 = 24%

$160,701 - $204,100 = 32%

$204,101 - $510,300 = 35%

$510,301 and over = 37%

Once we get more info about your income, we'll automatically calculate your rates and apply these changes to your refund.

How do tax brackets work?

Tax brackets show you the tax rate you'll pay on each portion of your income. For instance, as a taxpayer filing Single, the lowest tax rate of 10% is applied to the first $9,950 of your income in 2021. The next chunk of your income is then taxed at 12%, and so on, up to the top of your taxable income.

_is_anchored_off_the_coast_of_La_Brea%2C_Trinidad_and_Tobago._(48677005558).jpg/1920px-USNS_Comfort_(T-AH_20)_is_anchored_off_the_coast_of_La_Brea%2C_Trinidad_and_Tobago._(48677005558).jpg "Hospital ship USNS Comfort anchored off the coast of La Brea")

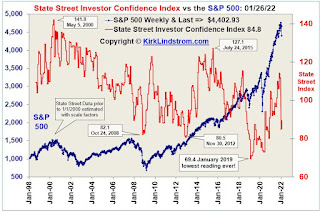

kirklindstrom.com

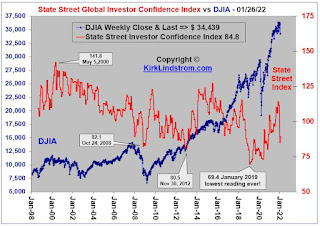

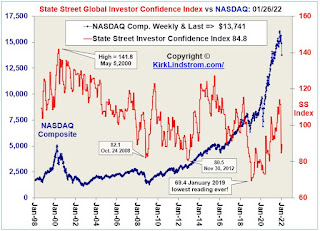

kirklindstrom.com