The following are the key proposals:

TAX RATES

Top marginal tax rate to go up from 37% to 39.6% effective for taxable years beginning

on or after December 31, 2021, and the 39.6% marginal tax rate would apply to taxable

income over $509,300 for married filing jointly and $452,700 for unmarried individuals.

These would be indexed for inflation after 2022.

CAPITAL GAINS

Major changes in capital gains taxation.

Currently, long term capital gains and qualified dividends are taxed at graduated rates

under the individual income tax with 20% being the highest rate (and, if applicable,

23.8% including the net investment income tax for those above certain modified adjusted

gross income).

- Capital gains are taxable only upon realization (i.e., Sale or other disposition of an appreciated asset).

- When a donor gives an appreciated asset to a donee during the donor’s life, the donor’s basis in the asset is the basis of the donor; in effect, the basis is carried over from the donor to the donee. There is no realization of capital gains by the donor at the time of the gift, and there is no recognition of capital gain or loss by the donee until the donee later disposes of that asset.

- When an appreciated asset is held by a decedent at death, the basis of the asset for the decedent’s heir is adjusted (stepped up) to the fair market value of the asset at the date of the decedent’s death. Thus, any appreciation accruing during the decedent’s life on assets that are still held by the decedent at death avoids federal income tax.

The proposal relating to capital gains taxation are as follows:

- Long term capital gains and qualified dividends of taxpayers with adjusted

gross income of more than $1 million would be taxed as ordinary income as high

as 43.4% including the net investment income tax, but only to the extent the

taxpayer’s income exceeds $1 million ($500,000 for married filing separately).

This would be indexed for inflation after 2022. The proposal says this would be

effective after the date of the announcement meaning late April 2021.

- Transfers of appreciated property by gift or on death will be treated as a

realization event. Under the proposal, the donor or deceased owner of an

appreciated asset would realize a capital gain at the time of the transfer. For

a donor, the amount of the gain realized would be the excess of the asset’s fair

market value on the date of the gift over the donor’s basis in that asset. For a

decedent, the amount of gain would be the excess of the asset’s fair market

value on the decedent’s date of death over the decedent’s basis in that asset.

The deemed owner of a revocable grantor trust would recognize gain on the

unrealized appreciation in any asset distributed from the trust to any person

other than the deemed owner or the U.S. spouse of the deemed owner.

- EXCEPTIONS:

a. Transfers to a U.S. spouse and charity – transfers by a decedent to a U.S. spouse or to a charity would carry over the basis of the decedent. Capital gains would not be recognized until the surviving spouse disposes the asset or dies. Distributions to charity will not generate a taxable gain. Transfers of appreciated assets to a split-interest trusts (i.e., CRUT, etc.) would generate a taxable capital gain with certain exclusions.

b. Transfers of tangible property (except collectibles) and principal residence would not trigger any gain. The $250,000 per person exclusion under current law for capital gain on a principal residence would continue to apply.

c. The Small Business Stock exclusion will continue to apply

d. In addition to the exclusions above, the proposal would allow a $1 million per person exclusion from recognition of other unrealized capital gains on property transferred by gift or held at death.

e. Payment of tax on the appreciation of certain family-owned and operated business would not be due until the interest in the business is sold or the business ceases to be family-owned and operated

f. The proposal would allow a 15-year fixed rate payment plan for the tax on appreciated assets transferred at death, other than liquid assets such as publicly traded financial assets and other than businesses for which the deferral election is made.

Currently, owners of appreciated real property used in a trade or business or held for

investments can defer gain on the exchange of the property for real property of a like

kind. As a result, the tax on the gain is deferred until a later recognition event, provided

that certain requirements are met.

The proposal, effective for exchanges completed in taxable years beginning after

December 31, 2021, would allow the deferral of gain up to an aggregate amount of

$500,000 for each taxpayer ($1 million in the case of married individuals filing a joint

return) each year for real property exchanges that are like kind. Any amounts in excess

would be taxable in the year the taxpayer transfers the real property subject to the

exchange.

3.8% MEDICARE TAX

Effective for taxable years beginning after December 31, 2021, the 3.8% Medicare Tax

will apply to all income and earnings over $400,000. In particular, for taxpayers with

adjusted gross income in excess of $400,000, the definition of net investment income tax

would be amended to include gross income and gain from any trades or businesses that

is not otherwise subject to employment taxes. Rules relating to limited partners and

LLC members are also being revised.

CARRIED INTEREST

The proposal would generally tax as ordinary income a partner’s share of income on an

“investment services partnership interest” in an investment partnership, regardless of the

character of the income at the partnership level, if the partner’s taxable income from all

sources exceed $400,000. Accordingly, such income would not be eligible for the

reduced rates that apply to long-term capital gains. The proposal also subjects this type

of income to self-employment tax.

CORPORATE TAX RATES

The proposal, effective for taxable years beginning after December 31, 2021, the income

corporate tax rate will rise from 21% to 28%.

OTHER KEY PROPOSALS

- Make permanent the American Rescue Plan Expansion of the Premium Tax Credits

- Make permanent the Expansion of the Earned Income Tax Credit for Workers without Qualifying Children

- Make permanent American Rescue Plan Changes to the Child and Dependent Tax Credit Daniel C. Moreno, CPA June 3, 2021

- Extend the Child Tax Credit Increase through 2025 and make permanent full refundability

- Make permanent excess business loss limitations of noncorporate taxpayers

- Implement additional funding for tax administration

- Introduce comprehensive financial accounting reporting to improve tax compliance

- Increase oversight of paid tax return preparers

- Enhance accuracy of tax information

- Expand broker information reporting with respect to Crypto assets

- Address taxpayer noncompliance with Listed Transactions

- Other administrative matters

- Various foreign, housing and infrastructure and energy related proposals

AREAS NOT ADDRESSED IN THE PROPOSALS

Surprisingly the following were not included in the proposal at this time:

- Elimination of the Section 199A 20% deduction on pass through income

- Setting a cap on itemized deduction at 28%

- Reducing the estate and gift tax exemption thresholds

- Eliminating the $10,000 cap on the state and local tax deductions.

This summary was prepared by an anonymous CPA who is about to retire, thus not looking for publicity or new clients.

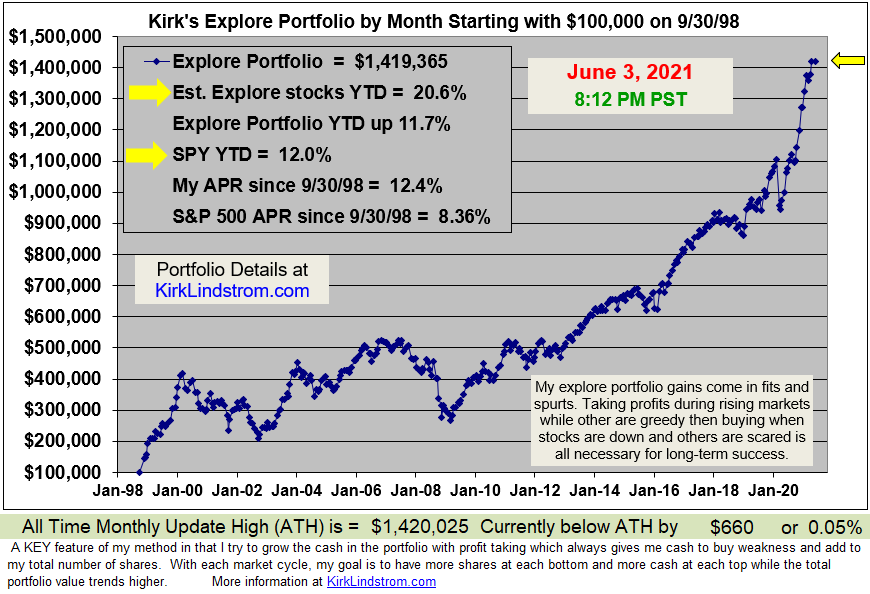

kirklindstrom.com

kirklindstrom.com