Despite the recent market volatility, this has been a great year to be invested in the US Stock market. This table shows that despite last month's market decline, the four major US indexes I track are up double digits:

As of 10/8/21, I hold 1,450 shares on "house money"

("break-even" includes dividends & XLRE spin-off which lowers the break-even point)

- Your 1 year, 12 issue subscription will start with next month's issue.

- Get email alerts when I buy or sell securities for my explore portfolio

- "Auto Buy" and "Auto

Sell" levels set ahead of time for target buy and sell

levels for my securities. This allows you to place

"limit orders" with your broker in advance so you can go

about your business.

- All questions about

what I write answered by Email. If what I write is not

clear to you, just ask!

- Only $180 per year via PayPal & $175 if you send a check.

It amazes me how many will pay a "financial advisor" fees as high as 2% a year to buy mutual funds for them (sometimes with high fees kicked back to the advisor) when you can do it yourself for the small cost of my newsletter. 2% a year for $100,000 under management over 10 years adds up.

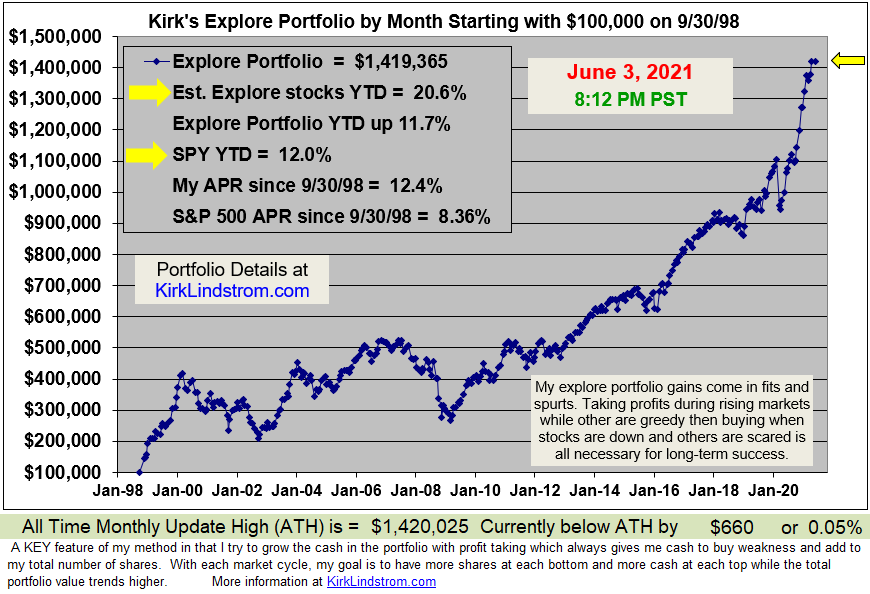

A major purpose of the Explore Portfolio is to help prevent you

from getting too greedy at market tops by taking profits or get

scared out near market bottoms by buying. For the last 20 years,

my Explore Stocks have also beaten the markets with far less risk

since the portfolio is far less than 100% in stocks. Like Warren

Buffett, I don't see loads of value near market tops and I like to

have a lot of cash for when the market presents great buying

opportunities. Great individual stock selection has greatly

enhanced the overall returns too.

kirklindstrom.com

kirklindstrom.com